A Complete, Step-by-Step Guide to Achieving Your Money Goals

Picture your perfect financial future. What do you see? Perhaps it’s a beautifully renovated home, paid in full. Maybe it’s the peace of mind that comes from a robust emergency fund. Or it’s the freedom to retire early and travel the world.

Now, look at your current bank balance. Does it align with that vision? For most people, the answer is “no.”

This gap—the space between where you are and where you want to be—is not an impassable chasm. It’s a road trip that requires a map. Without a destination, you are just driving in circles, wasting time and fuel (in this case, your hard-earned money).

Financial goal setting is your map. It is the process of defining your destination, plotting your course, and breaking the journey down into manageable, daily milestones. In this guide, we take the complex concept of “success” and make it a tangible, actionable plan. Let’s start plotting your route to financial freedom.

Financial goals are easier to achieve when your debts are under control.

Read our guide on

Smart Debt Management.

Table of Contents

- What Is Financial Goal Setting and Why Does It Matter?

- The Powerful Emotional and Financial Effects of Having a Goal

- Types of Financial Goals: Short, Medium, and Long-Term

- How to Create an Emergency Fund: Your First Financial Goal

- Step-by-Step Guide to Effective Financial Goal Setting

- The Importance of Smart Debt Management within Your Goals

- Tools and Techniques to Keep You on Track

- Common Pitfalls and How to Avoid Them

- Illustrative Instances: Goal Setting in Real Life

- Frequently Asked Questions (FAQs)

- Conclusion

What Is Financial Goal Setting and Why Does It Matter?

At its core, financial goal setting is simply deciding what you want to achieve with your money within a specific timeframe.

It sounds obvious, but you’d be surprised how many people cannot answer the simple question: “What is your #1 financial goal right now?” They might say “save money,” but they haven’t defined how much, for what, or by when.

Without goals, your money follows the “path of least resistance.” It flows towards everyday conveniences, small impulsions, and unexamined habits. Financial goal setting introduces intentionality.

Clarity Over Confusion

Goals are powerful because they provide clarity. Instead of wondering if you can afford a new car, you can check your budget and see if it aligns with your “Car Savings Fund” timeline. Instead of a vague anxiety about retirement, you have a concrete number to aim for.

Focus and Discipline

Goals transform money from an abstract concept into a concrete tool. When you are saving $500/month for a specific goal (like the down payment for a house), it becomes a game you are trying to win, not a sacrifice you are forced to make. This focus provides the discipline needed to say “no” to temporary wants in favor of long-term needs.

Control vs. Chaos

Ultimately, financial goal setting gives you control. A budget isn’t a restriction; it’s a spending plan. A goal isn’t a far-off dream; it’s a target you are actively working to hit. You move from being reactive to your finances (e.g., panicking over a sudden bill) to being proactive.

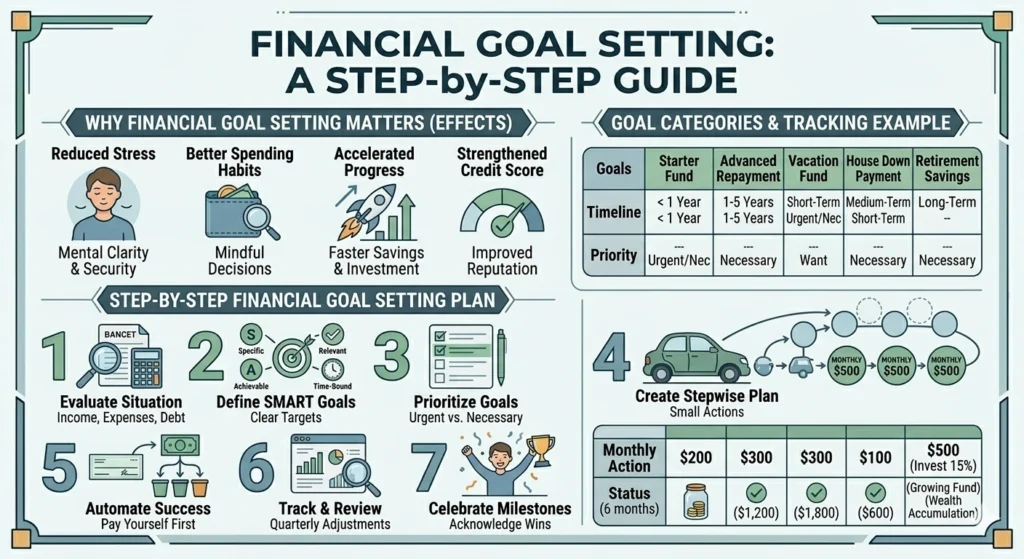

Strong Emotional & Financial Effects of Having a Goal

Setting a financial goal has immediate and tangible effects that go far beyond your bank statement.

[Illustration 1: A comparative image. On the left, a stressed person with thought bubbles of random expenses. On the right, a calm, focused person with a simple “GOAL” shield protecting a stack of coins and a rising graph, illustrating the mental clarity and security a goal provides.]

1. Reduced Financial Anxiety (The Mental Shield)

One of the most immediate effects is a reduction in stress. Uncertainty is a major source of anxiety. When you don’t have a plan, every unexpected expense feels like a potential catastrophe.

Once you have an emergency fund and a budget (both of which are financial goals), you have a “mental shield” that allows you to face surprises with calm confidence.

2. Mindful Spending Habits ( The Decision Filter)

Goals act as a powerful filter for your daily choices. Before you buy that $100 gadget or order an expensive dinner, you subconsciously (and sometimes consciously) ask: “Is this worth delaying my dream vacation?” A well-defined goal automatically encourages you to make more mindful and less impulsive decisions.

3. Accelerated Progress (The Compound Effect)

Intentionality is an accelerator. Randomly saving $50 here and there doesn’t build momentum. Consistently automating $300 a month towards a specific investment goal does. This momentum, combined with the power of compound interest, means that those with clear financial goals often build wealth much faster than those without them.

4. Strengthened Credit Score (The Reputation Bonus)

A common financial goal is debt repayment. Consistently paying down debt on time is the single most important factor in calculating your credit score. As you work towards the goal of being debt-free, your credit score rises as a “bonus effect,” opening doors to lower interest rates on mortgages, car loans, and insurance.

Types of Financial Goals: Short, Medium, and Long-Term

To manage your finances effectively, your goals must be categorized by their timeline. A goal to “buy a new laptop” is managed differently than a goal to “retire at 55.” Understanding this distinction prevents you from misallocating funds and feeling overwhelmed.

[Illustration 2: A simple, colored diagram showing three columns labeled “Short-Term (< 1 Yr)”, “Medium-Term (1-5 Yrs)”, and “Long-Term (5+ Yrs)”. Each column lists examples with unique icons, matching the visual style of image_0.png and image_2.png, to help users categorize their goals.]

1. Short-Term Financial Goals (< 1 Year)

These goals are about immediate needs, wants, and financial stability. They keep your finances running smoothly and allow for small victories.

- Saving for a Vacation: A specific, exciting target to aim for within the year.

- Creating a “Starter” Emergency Fund: Your absolute first priority. (See below for more details on this goal.)

- Paying Off Small Debts: Getting that $500 medical bill or old personal loan off your plate.

- Saving for a Gadget or Piece of Furniture: A defined purchase, like a new TV or sofa.

2. Medium-Term Financial Goals (1-5 Years)

These are larger life milestones that require consistent effort and structure over a longer period.

- Saving for a Down Payment on a House or Car: A significant cash reserve.

- Building a Fully Funded Emergency Fund: (3–6 months of living expenses).

- Starting a Small Side Business or Investment Portfolio: Building a new income stream or starting your wealth accumulation journey.

- Aggressively Paying Down Student or Personal Loans: Targeting debts that are costing you a lot in interest.

3. Long-Term Financial Goals (5+ Years)

These are foundational, lifetime goals that will define your financial future and legacy.

- Achieving Home Ownership: Securing your primary residence.

- Saving for Retirement: Building a substantial nest egg for the future. This is almost always an individual’s largest long-term goal.

- Funding Children’s Higher Education: Planning for a child’s college education costs.

- Becoming Completely Debt-Free: Including paying off your mortgage.

Crucial Note: A successful financial plan manages goals from all three categories simultaneously. You can (and should) be saving for a short-term vacation while building a medium-term emergency fund and investing for long-term retirement.

How to Create an Emergency Fund: Your First Financial Goal

If you have zero dollars in savings and are living paycheck to paycheck, your path is clear. Your very first financial goal is to build a “starter” emergency fund of $500–$1,000.

[Illustration 3: A minimalist, high-impact “Starter vs. Advanced Emergency Fund” chart, matching the clean-data aesthetic of image_0.png. It has two columns with illustrations of an emergency jar: a $500 “STARTER” jar and a 3-6 months “ADVANCED” jar, each with simple icons of common triggers (flat tire vs. medical bill/job loss) to clarify the difference between the goals.]

A “Starter” emergency fund isn’t about job loss or major medical bills. It’s a “catastrophe buffer.” It’s designed to cover small, common unexpected expenses—like a flat tire, a quick trip to the urgent care, or a broken microwave—that would otherwise send you into debt.

Step-by-Step Starter Fund Plan:

- Analyze Your Budget: Find $100 you can cut for one month (streaming services, dining out, unnecessary shopping).

- Sell Something: Find one unused item (old phone, clothes, furniture) and sell it online or at a garage sale.

- Find “Found” Money: Any unexpected income (rebate, birthday money, tax refund) goes immediately to this fund.

- Deposit it Immediately: Open a separate, high-yield savings account just for this fund. Do not touch it unless it is a true emergency.

Once you have this $500 buffer, you have crossed the starting line of financial goal setting. You can then begin working on the goals in the other categories, including the advanced goal of building a fully funded 3–6 month emergency fund.

Step-by-Step Guide to Effective Financial Goal Setting

You know what financial goal setting is, why it matters, and how to categorize your goals. Now, let’s get down to the actual work. Follow these steps to create a goal-setting plan that sticks.

Step 1: Evaluate Your Current Financial Situation

Before you can plan your route, you must determine your starting point. This is the most difficult step because it forces you to face uncomfortable numbers. Use our previous guide on budgeting to create an accurate monthly snapshot.

Your Goal baseline must include:

- Total Income (all sources)

- Total Fixed Expenses (rent, utilities, insurance)

- Total Variable Expenses (food, fun, shopping)

- Total Debt (list everything—type, balance, and interest rate)

- Total Savings (emergency fund, existing goals)

Understanding this baseline allows you to set goals that are challenging yet realistic for your unique situation.

Step 2: Define SMART Financial Goals

A goal that is vague will fail. To be effective, your goals must follow the S.M.A.R.T. criteria.

[Illustration 4: A beautifully designed infographic for the “S.M.A.R.T.” criteria for goal setting. It uses a modern flat design, with each letter (S, M, A, R, T) in its own distinct section, with simple icons and bold descriptions (Specific, Measurable, Achievable, Relevant, Time-Bound), using the teal and green color palette established in previous images to ensure visual continuity.]

S – Specific

Instead of “save more money,” make it: “Save money for a house down payment.”

M – Measurable

How much do you need? For our example, let’s say “$30,000.”

A – Achievable

Look at your baseline. Can you realistically achieve this in the next five years? If you are saving $500/month, you can hit $30,000 in 60 months. This goal is challenging but achievable.

R – Relevant

Does this goal align with your values and long-term vision? If home ownership is a top priority, then a down payment goal is incredibly relevant.

T – Time-Bound

When is your deadline? “We want to buy our house in five years (60 months).”

Result: A vague dream is transformed into a S.M.A.R.T. goal: “We will save $30,000 for a house down payment by automating $500 per month into a dedicated, high-yield savings account, with a target date of [Month, Year].”

Step 3: Prioritize Your Goals

You have multiple goals (e.g., save for a house, pay off debt, build an emergency fund, save for a vacation). You cannot work on all of them with the same level of focus. Look at our categorization list and prioritize them based on necessity, urgency, and impact.

For example, a prioritized list might look like this:

- [Urgent/Necessary] Starter Emergency Fund ($1,000). (Goal 1, Short-Term)

- [Necessary/Urgent] Fully Funded 3-Month Emergency Fund. (Goal 2, Medium-Term)

- [Necessary] High-Interest Debt Repayment. (Goal 3, Short-Term, see below)

- [Long-Term/Necessary] Increase Retirement Contributions. (Goal 4, Long-Term)

- [Want/Short-Term] Save $2,000 for a summer vacation. (Goal 5, Short-Term)

Step 4: Create an Actionable, Stepwise Plan

This is where you break your big goal down into tiny, daily actions. A $30,000 house down payment can feel paralyzing. $500 a month feels like something you can manage.

[Illustration 5: A clear flow-chart illustration “CREATING AN ACTIONABLE, STEPWISE PLAN”. It breaks down a large goal (e.g., “Save $6,000 for a Car in 12 Months”) into smaller, circular steps: “SET TARGET: $6,000”, “CALCULATE MONTHLY: $500”, “FIND $500: CUT EXPENSES + ADD INCOME”, and “DEPOSIT MONTHLY: AUTOMATE IT!”. Uses clean icons of cars, money piles, and calculators, maintaining the modern digital graphic style of previous images.]

Break your prioritized goals into monthly actions:

- Goal 1: Starter Emergency Fund. Save $200/month (achieved in 5 months).

- Goal 2: Advanced Emergency Fund. Save $300/month (ongoing).

- Goal 3: Debt Repayment. Automate extra payments of $300/month (ongoing).

- Goal 4: Vacation Fund. Automate $100/month (achieved in 20 months).

You now have an action plan that requires you to automate total monthly savings of $900 ($200 + $300 + $300 + $100). If this exceeds your available cash, you must go back to prioritizing or adjust your deadlines.

Step 5: Automate Your Success

Automation is the “secret sauce” of successful financial goal setting. It is the single most effective way to guarantee consistency.

Set up an automatic transfer from your checking account to your savings/investment accounts for each goal, preferably on the same day you get paid. This ensures that you “pay yourself first,” and your goal contributions never become an afterthought. By making it hands-off, you remove the temptation to spend the money before you save it.

Step 6: Track and Review Regularly

Your plan is a dynamic document, not a rigid contract. Review your goals quarterly to ensure you are on track and make adjustments as life changes. If you get a raise, increase your goal contributions. If you face a setback, adjust your deadlines. Constant tracking keeps you accountable and motivated.

Step 7: Celebrate Milestones

The road to a $30,000 down payment is long. Celebrate small wins to keep your motivation high. When you hit $5,000, $10,000, or cross the 1-year mark of consistent saving, acknowledge your progress. Treat yourself to a small, inexpensive reward that doesn’t detail your goals. Recognizing progress is essential for building sustainable financial habits.

The Importance of Smart Debt Management within Your Goals

You cannot build wealth effectively while you are chained to debt. A smart financial goal plan must address debt, particularly high-interest consumer debt (like credit cards or personal loans). Look at your prioritized goal list: you’ll notice “High-Interest Debt Repayment” is always at or near the top.

[Illustration 6: A multi-column illustrative graphic, “SMART DEBT MANAGEMENT IN YOUR GOALS”, matching the structured infographic style of image_2.png. It features three columns with simple icons and summaries:

- The Debt Drag: A frustrated person with a small weight on their ankle, labeling “Ignoring Debt = Slow Growth”, with an icon of growing interest.

- Prioritize Repayment: A checkmark and a calendar, labeling “Top of your prioritized goals” (Urgent/Necessary).

- Debt-Freedom Effects: A calm, strong person breaking free, labeling “Reduced Interest Costs”, “Better Credit Score”, “Financial Freedom.” All columns use the established teal, green, and blue color palette.]

Ignore debt and it acts as a “drag” on every other financial aspiration. A goal to save $500 a month for a house down payment will have limited impact if you are paying $300 a month in credit card interest.

We dedicated a full previous guide to this topic, but here are the key intersections with goal setting:

- Prioritize Debt Repayment: If you have high-interest debt (over 7–8%), make paying it down a top-tier, “Necessary” goal. Use a strategy like the Debt Avalanche (highest interest first) or Debt Snowball (smallest balance first).

- Use Windfalls for Debt: A tax refund, gift money, or bonus should first go to your starter emergency fund and then to high-interest debt.

- Align Debt Freedom with Large Goals: A goal to become debt-free (e.g., in 3 years) should align with your next big milestones, such as buying a house or increasing retirement contributions.

Tools and Techniques to Keep You on Track

You don’t have to do this alone. Use tools to simplify the process and charts to visualize your success.

Visual Progress Charts ( The Ultimate Motivator)

There is nothing more satisfying than visually seeing a goal become a reality. Create a simple “Goal Tracking Chart” to monitor your progress.

Example Goal tracking Chart:

Goal: New Laptop $1,200 | Timeline: 6 months

[A visualization of this chart: A stack of six laptop icons, one for each month, with the first three fully colored with green checkmarks, showing progress.]

| Month | Target Amount | Extra Contribution | Progress status |

| Month 1 | $200 | ✅ ($200) | [Checkmark] |

| Month 2 | $200 | ✅ ($200) | [Checkmark] |

| Month 3 | $200 | ✅ ($200) | [Checkmark] |

| Month 4 | $200 | [Empty] | |

| Month 5 | $200 | [Empty] | |

| Month 6 | $200 | [Empty] | |

| Total | $1,200 |

Budgeting Apps and Spreadsheets ( The Data Source)

Use a budgeting app (YNAB, Mint) or a simple spreadsheet to get the accurate data you need for Step 1 of the goal-setting process.

Common Pitfalls and How to Avoid Them

Why do financial goals fail? It’s often not a lack of money, but a lack of planning.

- Setting Unrealistic Goals: Look at your baseline. A goal to save $1,000/month when you only have $100 left is a recipe for discouragement. Start small and adjust deadlines.

- Failing to Prioritize: Randomly working on five different goals will yield slow results. Focus your extra money on one or two top priorities.

- Not Automating Savings: Relying on willpower alone fails. Automation guarantees consistency.

- A “Set and Forget” Mentality: Life changes. If you don’t review your goals regularly, your plan will become irrelevant to your current needs.

- Letting Emotions Drive Spending: Emotional, impulsive spending is the enemy of goal setting. Goals introduce intentionality, but you must consistently apply that “Decision Filter.”

Illustrative Instances: Goal Setting in Real Life

Let’s look at two instances of how this process works.

Instance 1: The Credit Card Debt Smasher (Sarah)

Sarah, 26, accumulated $4,500 in credit card debt after an unexpected move. It was causing her stress.

- Evaluate: CC Debt: $4,500 at 22% interest. She had $300 “extra” each month.

- Prioritize: Sarah prioritized debt freedom as her #1 urgent/necessary goal.

- Plan: She automated a monthly payment of $300.

- Effects: In just 15 months, she was debt-free, saving herself hundreds in interest. This win boosted her confidence and freed up $300 a month that she then applied to her next goal: building a fully funded emergency fund.

Instance 2: The First-Time Home Buyer (Mark & Emily)

Mark and Emily, a couple in their early 30s, wanted to buy a home.

- Evaluate: CC Debt: $0. Starter Emergency Fund: $1,000. Combined Extra: $900/month.

- SMART Goal: Save $30,000 for a down payment in 5 years (60 months) by automating $500/month.

- Prioritize: While focusing $500/month on the house, they continued investing 15% in retirement (long-term goal) and put $200/month into an advanced emergency fund (medium-term goal), leaving $200/month for fun/discretionary spending.

- Automation: They automated the $500 transfer to a dedicated “House Fund” account.

- Tracking: In just 3 years, they had $18,000. They received a $2,000 windfall and put it directly into the fund. They hit their goal and bought their first home.

10 Frequently Asked Questions (FAQs)

1. How many financial goals should I set?

Start with 3–5 goals across different categories (short, medium, and long-term) to maintain focus.

2. Should I prioritize paying off debt or saving money?

Prioritize building a “Starter” emergency fund of $500–$1,000 first. Once you have that, focus your extra cash on paying off high-interest debt (over 7–8%).

3. Is it possible to set financial goals on a low income?

Yes. Even small contributions (e.g., $25/month) make progress. The goal is to build the habit of consistent saving and automation.

4. How can I stay motivated to save for a goal that is 10 years away?

Focus on smaller, exciting short and medium-term goals. Celebrate milestones along the way and visualize your long-term success.

5. Should I involve my partner/spouse in goal setting?

Yes. Shared financial goals strengthen relationships and improve accountability for shared expenses.

6. Can I change or adjust my goals?

Absolutely. Review your goals quarterly and adjust deadlines or targets as life changes (new job, raise, unexpected expense). Goals should be flexible, not rigid.

7. How do I choose between the Debt Snowball and Avalanche method?

Snowball (smallest balance first) is better for motivation. Avalanche (highest interest first) is mathematically optimal. The most important thing is choosing a method and sticking to it.

8. Should my emergency fund be in its own account?

Yes. Keep your emergency savings in a separate, high-yield savings account (HYSA) so you are not tempted to spend it.

9. What if I face a setback and cannot make my automated transfer?

Do not panic. Adjust the transfer down for that one month. A small contribution is always better than zero. The key is to remain disciplined once the emergency passes.

10. What happens after I achieve all my current goals?

Revisit your categorization chart. Create new long-term goals (e.g., early retirement) or focus on maximizing your current investments. The goal-setting process is a virtuous cycle.

Conclusion

Financial goal setting is not a magic trick. It is a structured process that transforms your abstract dreams into concrete, daily actions. It is the roadmap that guides your money away from daily drift and towards lifetime success.

Remember, you are not alone. By using charts, automating your transfers, and following the steps in this guide—evaluating your situation, defining SMART goals, and prioritizing your actions—you can secure your finances, reduce your stress, and secure a brighter future.

A virtuous cycle has already begun. You have learned how to build an emergency fund, prioritize debt, and set meaningful, achievable money goals.

Don’t wait. Start today by setting one small, short-term goal that you can achieve in the next month. Small steps, taken consistently, lead to massive financial transformation.

You can also stretch your money further using

Frugal Living Tips.