A Practical Guide to Taking Control of Your Finances

Debt is a common part of modern life. Many people rely on loans, credit cards, or financing to pay for education, homes, vehicles, or unexpected expenses. While borrowing money can sometimes help achieve important goals, unmanaged debt can quickly become a serious financial burden.

This is why smart debt management is essential.

Smart debt management means using effective strategies to control, reduce, and eliminate debt while maintaining financial stability. Instead of feeling overwhelmed by payments and interest rates, you create a structured plan that allows you to gradually regain control of your finances.

Many people assume debt freedom requires earning a large income or making extreme sacrifices. In reality, successful debt management often comes from simple but consistent financial habits such as budgeting, prioritizing repayments, and avoiding unnecessary borrowing.

In this complete guide, you will learn:

- What smart debt management really means

- The different types of debt and how they affect your finances

- Step-by-step strategies to manage debt effectively

- Practical charts and examples

- Real-life instances of successful debt reduction

- Common mistakes to avoid

- Frequently asked questions about debt management

By the end of this guide, you will have a clear roadmap to manage your debt wisely and build a stronger financial future.

Before tackling debt aggressively, make sure you have an

Emergency Fund to protect your finances.

Table of Contents

- Understanding Smart Debt Management

- Types of Debt You Should Know

- Why Managing Debt Properly Is Important

- Step-by-Step Smart Debt Management Plan

- Debt Repayment Methods Explained

- Debt Reduction Chart Example

- Real-Life Instances of Smart Debt Management

- Common Debt Management Mistakes

- Effects of Poor Debt Management

- Benefits of Smart Debt Management

- Tips to Stay Debt-Free Long-Term

- Frequently Asked Questions

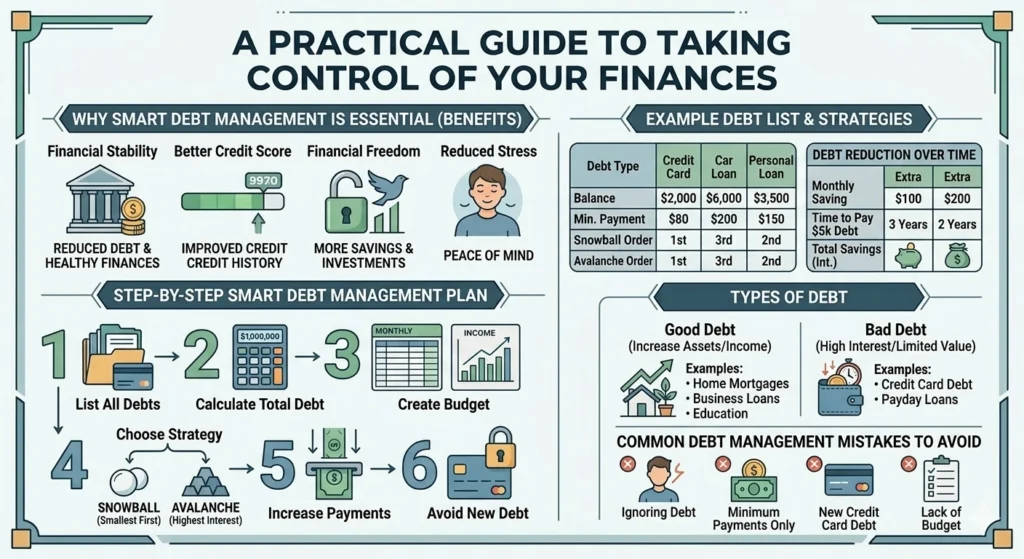

Understanding Smart Debt Management

Smart debt management is the process of controlling and reducing debt strategically while maintaining financial balance.

Instead of ignoring debts or making random payments, smart debt management focuses on:

- Understanding how much you owe

- Creating a structured repayment plan

- Reducing interest costs

- Avoiding unnecessary new debt

The goal is not just to pay off debt but also to build healthier financial habits for the future.

Types of Debt You Should Know

Not all debts are the same. Understanding different types of debt helps you manage them more effectively.

Good Debt

Good debt often helps improve long-term financial opportunities.

Examples include:

- Education loans

- Home mortgages

- Business loans

These debts can increase income potential or asset value.

Bad Debt

Bad debt usually involves high interest and limited long-term value.

Examples include:

- Credit card debt

- Payday loans

- High-interest personal loans

Bad debt often grows quickly if not managed carefully.

Secured Debt

Secured debt is backed by collateral.

Examples include:

- Car loans

- Mortgages

If payments stop, the lender can seize the asset.

Unsecured Debt

Unsecured debt has no collateral.

Examples include:

- Credit cards

- Personal loans

These debts often carry higher interest rates.

Why Managing Debt Properly Is Important

Poor debt management can cause serious financial problems.

Financial Stress

Constant debt payments create pressure and anxiety.

High Interest Costs

Interest can significantly increase the total amount owed.

Limited Financial Freedom

Too much debt reduces your ability to save or invest.

Credit Score Damage

Missed payments can harm your credit history.

Smart debt management helps avoid these risks and creates a path toward financial stability.

Step-by-Step Smart Debt Management Plan

Following a structured process makes debt repayment more manageable.

Step 1: List All Your Debts

Start by creating a complete list of everything you owe.

Example chart:

| Debt Type | Balance | Interest Rate | Minimum Payment |

|---|---|---|---|

| Credit Card | $2,000 | 20% | $80 |

| Car Loan | $6,000 | 8% | $200 |

| Personal Loan | $3,500 | 12% | $150 |

This overview helps you understand your financial situation.

Step 2: Calculate Your Total Debt

Add all outstanding balances.

Example:

$2,000 + $6,000 + $3,500 = $11,500 total debt

Knowing the exact amount helps create a realistic repayment strategy.

Step 3: Create a Monthly Budget

Budgeting ensures you have money available for repayments.

Example:

| Income | Amount |

|---|---|

| Monthly salary | $2,500 |

| Expenses | Amount |

|---|---|

| Rent | $900 |

| Food | $300 |

| Transport | $200 |

| Utilities | $150 |

Remaining amount for debt payments = $950

Step 4: Choose a Debt Repayment Strategy

Two popular methods help reduce debt faster.

Debt Snowball Method

Pay the smallest debts first.

Example order:

- Credit card ($2,000)

- Personal loan ($3,500)

- Car loan ($6,000)

This method builds motivation through quick wins.

Debt Avalanche Method

Pay debts with the highest interest first.

Example order:

- Credit card (20%)

- Personal loan (12%)

- Car loan (8%)

This method saves more money on interest.

Step 5: Increase Monthly Payments

Paying more than the minimum reduces debt faster.

Example:

| Payment Strategy | Time to Pay Off $5,000 Debt |

|---|---|

| Minimum payments | 6 years |

| Extra $100 monthly | 3 years |

| Extra $200 monthly | 2 years |

Small increases can significantly shorten repayment time.

Step 6: Avoid New Debt

While paying off existing debt, avoid new borrowing whenever possible.

Strategies include:

- Limiting credit card usage

- Using cash for purchases

- Creating a spending plan

Debt Reduction Chart Example

The following chart shows how consistent payments reduce debt.

| Month | Debt Balance |

|---|---|

| Month 1 | $5,000 |

| Month 3 | $4,300 |

| Month 6 | $3,500 |

| Month 12 | $2,100 |

Steady progress builds confidence and financial stability.

Real-Life Instances of Smart Debt Management

Instance 1: Credit Card Debt Elimination

Sarah accumulated $4,500 in credit card debt.

She applied the snowball method:

- Reduced dining expenses

- Added $200 extra monthly payment

Result:

Debt paid off in 18 months instead of 4 years.

Instance 2: Family Debt Recovery

A family with $20,000 in combined debt created a strict repayment plan.

Actions taken:

- Cancelled unnecessary subscriptions

- Started a small side business

- Paid $700 monthly toward debt

Outcome:

Debt eliminated in 3 years.

Common Debt Management Mistakes

Many people struggle with debt because of avoidable mistakes.

Ignoring Debt Problems

Avoiding debt often leads to higher interest and penalties.

Making Only Minimum Payments

Minimum payments slow down progress.

Using Credit Cards for Everyday Spending

This can increase debt quickly.

Lack of Budget Planning

Without a budget, repayment strategies fail.

Effects of Poor Debt Management

Poor debt habits can cause long-term consequences.

Financial Effects

- Increased interest payments

- Difficulty saving money

- Limited investment opportunities

Emotional Effects

- Financial anxiety

- Stress in relationships

- Reduced confidence in financial decisions

Benefits of Smart Debt Management

When you manage debt effectively, several positive outcomes occur.

Financial Stability

Reduced debt improves overall financial health.

Better Credit Score

Consistent payments strengthen credit history.

More Financial Freedom

Less debt means more money for savings and investments.

Reduced Stress

Financial control improves peace of mind.

Tips to Stay Debt-Free Long-Term

Even after paying off debt, maintaining discipline is important.

Build an Emergency Fund

Emergency savings prevent borrowing during unexpected events.

Track Spending

Monitoring expenses helps prevent overspending.

Use Credit Responsibly

Only borrow money when necessary.

Increase Financial Education

Understanding money management improves decision-making.

Frequently Asked Questions

1. What is smart debt management?

Smart debt management involves organizing, reducing, and controlling debt through budgeting, structured repayment plans, and responsible borrowing.

2. What is the best way to pay off debt?

The most common methods are the debt snowball and debt avalanche strategies.

3. Can I manage debt with a low income?

Yes. Even small extra payments can gradually reduce debt over time.

4. Should I stop using credit cards completely?

Not necessarily. Responsible usage can help maintain a healthy credit score.

5. What happens if I miss a debt payment?

Missed payments can lead to late fees, higher interest, and credit score damage.

6. How long does it take to become debt-free?

The timeline depends on your debt amount, income, and repayment strategy.

7. Is consolidating debt a good idea?

Debt consolidation can simplify payments but should be evaluated carefully.

8. Should I save money while paying off debt?

Yes. Even a small emergency fund can prevent further borrowing.

9. How can I avoid falling back into debt?

Maintain a budget, control spending, and prioritize savings.

10. Does paying off debt improve credit score?

Yes. Lower debt balances and consistent payments strengthen credit history.

Final Thoughts

Debt does not have to control your financial life. With the right knowledge and consistent actions, anyone can manage and reduce debt successfully.

Smart debt management focuses on understanding your financial obligations, creating a structured repayment plan, and avoiding unnecessary borrowing.

By applying the strategies in this guide, you can gradually reduce your debt, improve your financial stability, and move closer to long-term financial freedom.

Remember: small steps taken consistently can lead to major financial transformation.

Personal Debt Repayment Tracker

“The journey to financial freedom starts with a single payment.”

| Debt Name | Total Balance | Interest Rate | Min. Payment | Goal Payoff Date |

| Ex: Credit Card A | $2,000 | 18% | $60 | Dec 2026 |

Monthly Progress Log

Use this to track your total debt decreasing month by month.

| Month | Total Debt Remaining | Extra Payment Made | Milestone Reached? |

| Month 1 | $ | $ | [ ] |

| Month 2 | $ | $ | [ ] |

| Month 3 | $ | $ | [ ] |

| Month 4 | $ | $ | [ ] |

After managing debt, the next important step is setting clear

Financial Goals.

Which Strategy Are You Using?

- [ ] Debt Snowball: (Smallest balance first for quick wins)

- [ ] Debt Avalanche: (Highest interest rate first to save money)

Take Possessions.