Introduction

Loans can be powerful financial tools when used wisely. They help individuals and businesses achieve goals such as buying a home, expanding a business, funding education, or handling emergencies. However, without proper planning and discipline, loans can quickly become a burden, leading to high interest payments, financial stress, and long-term debt cycles.

Smart loan management is not just about borrowing money—it is about borrowing strategically, repaying efficiently, and maintaining financial stability. This guide provides a complete, practical, and SEO-optimized approach to managing loans effectively. Whether you are dealing with personal loans, business loans, student loans, or mortgages, these strategies will help you stay in control.

Table of Contents

- Understanding Loans

- Why Smart Loan Management Matters

- Types of Loans and Their Uses

- Core Principles of Smart Loan Management

- Loan Planning Before Borrowing

- Interest Rates Explained

- Loan Repayment Strategies

- Debt Reduction Techniques

- Loan Comparison Table

- Real-Life Examples

- Common Mistakes to Avoid

- Loan Management Tools and Tips

- Financial Security and Loans

- When to Take a Loan (and When Not To)

- Summary

- FAQs

Understanding Loans

What is a Loan?

A loan is money borrowed from a financial institution or lender that must be repaid over time, usually with interest.

Key Loan Terms

| Term | Meaning |

|---|---|

| Principal | Amount borrowed |

| Interest Rate | Cost of borrowing |

| Loan Term | Repayment period |

| EMI/Installment | Fixed monthly payment |

| Default | Failure to repay |

Understanding these terms helps you make informed decisions.

Why Smart Loan Management Matters

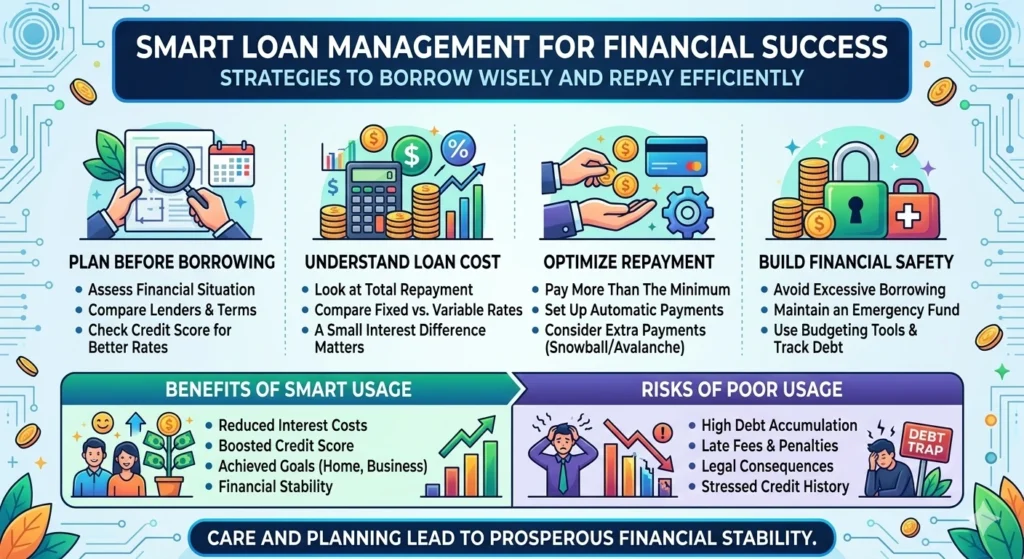

Poor loan management can lead to financial hardship. Smart management ensures:

Benefits

- Reduced financial stress

- Lower interest payments

- Improved credit score

- Better financial planning

Risks of Poor Management

- High debt accumulation

- Penalties and late fees

- Legal consequences

- Damaged credit history

Types of Loans and Their Uses

Common Loan Types

| Loan Type | Purpose |

|---|---|

| Personal Loan | General expenses |

| Mortgage | Buying property |

| Auto Loan | Vehicle purchase |

| Student Loan | Education |

| Business Loan | Business growth |

Each loan type has different terms and interest rates, so understanding them is essential.

Core Principles of Smart Loan Management

Borrow Only What You Need

Avoid taking more than necessary. Extra borrowing increases repayment pressure.

Understand Total Loan Cost

Look beyond monthly payments and calculate total repayment.

Keep Loan-to-Income Ratio Low

Your loan repayments should not exceed 30–40% of your income.

Loan Planning Before Borrowing

Assess Your Financial Situation

Ask yourself:

- Can I afford monthly payments?

- Is this loan necessary?

Compare Multiple Lenders

Never accept the first offer. Compare:

- Interest rates

- Repayment terms

- Fees

Check Your Credit Score

A higher credit score gives:

- Lower interest rates

- Better loan options

Interest Rates Explained

Fixed vs Variable Interest Rates

| Type | Description |

|---|---|

| Fixed | Same throughout loan |

| Variable | Changes over time |

Example

| Loan Amount | Interest Rate | Total Repayment |

|---|---|---|

| $5,000 | 10% | Higher total |

| $5,000 | 5% | Lower total |

Even a small difference in interest rates can significantly affect total cost.

Loan Repayment Strategies

Pay More Than the Minimum

Paying extra reduces:

- Interest costs

- Loan duration

Use the Snowball Method

- Pay smallest loan first

- Move to larger debts

Use the Avalanche Method

- Pay highest interest loan first

- Save more money over time

Automate Payments

Ensures:

- No missed deadlines

- Better credit score

Debt Reduction Techniques

Consolidation

Combine multiple loans into one.

Benefits:

- Simpler payments

- Lower interest (sometimes)

Refinancing

Replace your loan with a better one.

Benefits:

- Lower interest rate

- Better terms

Loan Comparison Table

| Factor | Good Loan | Bad Loan |

|---|---|---|

| Interest Rate | Low | High |

| Terms | Flexible | Rigid |

| Fees | Minimal | High |

| Transparency | Clear | Hidden |

Real-Life Examples

Example 1: Smart Borrower

- Takes a loan within income limit

- Pays more than minimum

- Clears loan early

Result: Saves money and improves credit score

Example 2: Poor Borrower

- Borrows excessively

- Misses payments

- Ignores interest rates

Result: Debt accumulation and financial stress

Common Mistakes to Avoid

- Borrowing without a plan

- Ignoring interest rates

- Missing payments

- Taking multiple loans at once

- Not reading loan terms

Loan Management Tools and Tips

Use Budgeting Tools

Track:

- Income

- Expenses

- Loan payments

Set Financial Goals

Clear goals help you stay disciplined.

Build Emergency Fund

Helps avoid borrowing in urgent situations.

Financial Security and Loans

Loans should not compromise your financial safety.

Tips

- Avoid over-borrowing

- Maintain savings

- Keep insurance where necessary

When to Take a Loan

- For productive purposes (business, education)

- When necessary and affordable

When to Avoid Loans

- For luxury or impulse spending

- When income is unstable

- When already in debt

Smart Loan Management Strategies (Advanced)

Early Repayment Strategy

Pay off loans early to reduce total cost.

Bi-Weekly Payment Plan

Instead of monthly payments:

- Pay every two weeks

- Reduces interest over time

Loan vs Credit Card Debt

| Feature | Loan | Credit Card |

|---|---|---|

| Interest | Lower | Higher |

| Structure | Fixed | Flexible |

| Risk | Moderate | High |

Building a Long-Term Loan Strategy

- Plan before borrowing

- Track all debts

- Prioritize high-interest loans

- Stay disciplined

Summary

Smart loan management is essential for financial stability. It involves careful planning, disciplined repayment, and informed decision-making.

Key takeaways:

- Borrow only what you need

- Understand interest rates

- Pay more than minimum

- Avoid unnecessary debt

- Monitor your financial health

When managed properly, loans can help you grow financially instead of holding you back.

Frequently Asked Questions (FAQs)

1. What is smart loan management?

It is the process of borrowing and repaying loans efficiently to minimize cost and risk.

2. How can I reduce loan interest?

Pay extra, refinance, or choose lower-interest loans.

3. Is it good to take multiple loans?

Only if you can manage repayments comfortably.

4. What is the best repayment strategy?

Avalanche method saves more money; snowball builds motivation.

5. Can I repay my loan early?

Yes, but check for prepayment penalties.

6. How much loan can I afford?

Keep repayments within 30–40% of your income.

7. What happens if I miss a payment?

You may face penalties and credit score damage.

8. Should I consolidate loans?

Yes, if it reduces interest and simplifies payments.

9. What is refinancing?

Replacing your loan with a better one.

10. Are loans good or bad?

They are good when used wisely and repaid responsibly.