Master Your Money

Imagine standing in front of a massive, high-tech vending machine in the year 2026. This machine doesn’t just sell snacks; it sells “Future You.” One button offers a comfortable retirement, another offers a debt-free home, and a third offers the freedom to quit your job and travel the world. The catch? The machine doesn’t take cash or cards. It only accepts a currency called Financial Literacy.

In a world where digital currencies, AI-driven stock bots, and “Buy Now, Pay Later” (BNPL) schemes are the norm, understanding the basics of money isn’t just a “nice-to-have” skill—it’s a survival mechanism. Whether you are a Gen Z professional navigating your first salary or a seasoned worker realizing that 2025’s inflation changed the rules of the game, this guide is your roadmap. We are moving beyond simple “penny-pinching” and into the realm of Mindful Wealth.

Table of Contents

- What is Financial Literacy in 2026?

- The 5 Pillars of Personal Finance

- Pillar 1: Masterful Budgeting (The 50/30/20 Rule & Beyond)

- Pillar 2: The Fortress of Savings (Emergency Funds)

- Pillar 3: The Debt Trap vs. The Debt Tool

- Pillar 4: Credit Scores: Your Financial Reputation

- Pillar 5: Investing: The Engine of Wealth

- 2026 Trends: Mindful Spending & Digital Banking

- Common Financial Pitfalls to Avoid

- Comparative Analysis: Traditional vs. Modern Strategies

- Your 7-Step Action Plan for Financial Freedom

- Frequently Asked Questions

- Summary: The Road Ahead

What is Financial Literacy in 2026?

Financial literacy is the ability to understand and effectively use various financial skills, including personal financial management, budgeting, and investing. But in 2026, it has evolved. It’s no longer just about balancing a checkbook (does anyone even use those anymore?).

Today, being financially literate means you can decode the hidden fees in a “Zero-Interest” BNPL offer, you understand how rising interest rates in the Eurozone or the US affect your mortgage, and you know how to leverage AI tools to automate your savings without losing track of where your money is going.

According to recent 2026 data, over 53% of adults report increased financial stress due to the rising cost of living, yet 76% feel optimistic that they can improve their situation with the right knowledge. That gap—between stress and optimism—is where financial literacy lives. It transforms “money anxiety” into “money agency.”

The 5 Pillars of Personal Finance

To build a skyscraper, you need a solid foundation. To build wealth, you need these five pillars.

Pillar 1: Masterful Budgeting

Budgeting is not about restriction; it’s about allocation. It’s telling your money where to go instead of wondering where it went. In 2026, we advocate for “Balanced Expense Management.”

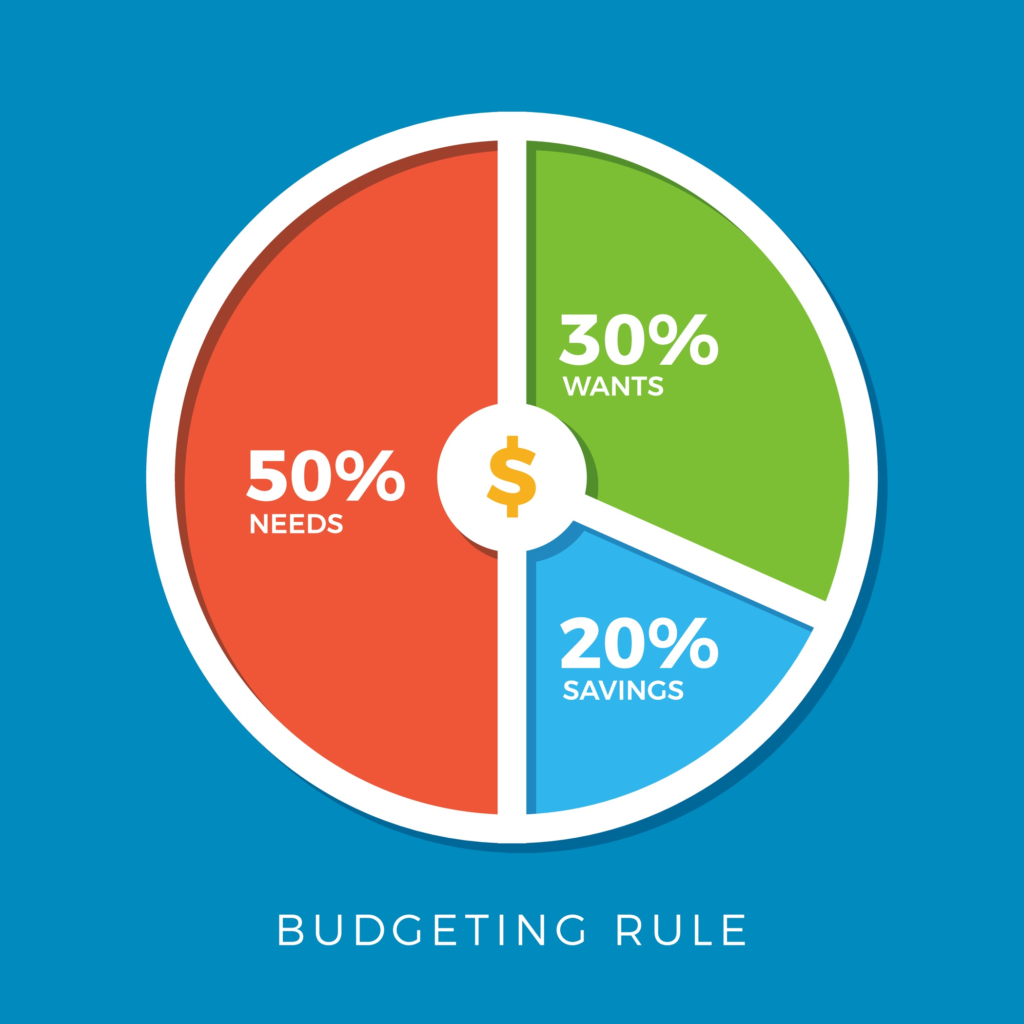

The 50/30/20 Rule

This is the gold standard for beginners. It splits your after-tax income into three buckets:

- 50% for Needs: Rent/Mortgage, utilities, groceries, insurance, and minimum debt payments.

- 30% for Wants: Dining out, Netflix, hobbies, and that “Little Treat” culture that 2026 is famous for.

- 20% for Financial Goals: Savings, extra debt payments, and investments.

Example: If you take home $4,000 a month:

- $2,000 goes to survival.

- $1,200 goes to enjoying life.

- $800 goes to your future.

Pillar 2: The Fortress of Savings

If 2025 taught us anything, it’s that “unprecedented events” happen every Tuesday. An Emergency Fund is your insurance policy against life.

- The Goal: 3 to 6 months of essential living expenses.

- Where to Keep It: A High-Yield Savings Account (HYSA) or a Money Market Account. In 2026, digital banks often offer significantly higher rates (around 4.5% to 5.0%) compared to traditional brick-and-mortar banks (often stuck at 0.01%).

Why it matters: If your car breaks down and it costs $1,200 to fix, an emergency fund makes it a “minor inconvenience.” Without one, that $1,200 goes on a credit card at 24% interest, turning a bad day into a months-long financial disaster.

Pillar 3: The Debt Trap vs. The Debt Tool

Not all debt is created equal. Understanding the difference between “Good Debt” and “Bad Debt” is a hallmark of the financially literate.

- Good Debt: Typically has low interest rates and is used to purchase assets that grow in value (e.g., a mortgage or a student loan for a high-ROI degree).

- Bad Debt: High-interest debt used for depreciating assets (e.g., credit card debt for clothes, or high-interest payday loans).

Debt Repayment Strategies: Snowball vs. Avalanche

| Strategy | Method | Psychological Impact | Best For |

|---|---|---|---|

| Debt Snowball | Pay off the smallest balance first, regardless of interest. | High (Quick wins build momentum). | People who need motivation. |

| Debt Avalanche | Pay off the highest interest rate first. | Low (Takes longer to see a “zero”). | People who want to save the most money. |

Pillar 4: Credit Scores: Your Financial Reputation

Your credit score is a three-digit number that tells lenders how “risky” you are. In 2026, your score doesn’t just affect loans; it can affect your insurance premiums and even your ability to rent a high-end apartment.

Factors that influence your score:

- Payment History (35%): Do you pay on time?

- Credit Utilization (30%): Are you using more than 30% of your available limit?

- Length of Credit History (15%): How long have you had accounts?

- Credit Mix (10%): Do you have different types of credit (cards, auto, etc.)?

- New Credit (10%): Have you opened too many accounts lately?

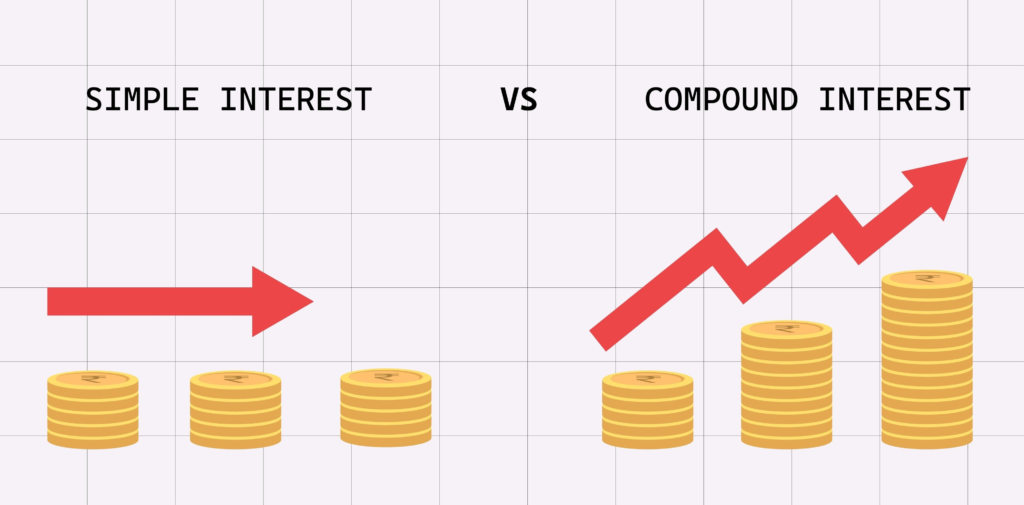

Pillar 5: Investing: The Engine of Wealth

If saving is putting money in a box, investing is planting a seed that grows into a tree. The most powerful tool here is Compound Interest.

As Einstein supposedly said, “Compound interest is the eighth wonder of the world.” It’s the process where your interest earns interest.

The Math of Growth:

Imagine you invest $500 a month starting at age 25. With a 7% average annual return, by age 65, you’d have roughly $1.2 million. If you wait until age 35 to start, you’d have only $580,000. That 10-year delay cost you over $600,000!

2026 Trends: Mindful Spending & Digital Banking

The landscape of money changed drastically in the mid-2020s. Two major trends dominate the 2026 financial discourse:

1. The “Little Treat” vs. Mindful Spending

We’ve moved away from the “no lattes” era. In 2026, 49% of consumers practice Mindful Spending. This means you intentionally cut back on things that don’t bring joy (like unused subscriptions or overpriced insurance) so you can afford “High-Impact Spending” (like a meaningful vacation or a high-quality hobby). It’s “Financial Gymnastics”—being frugal on Tuesday so you can be fabulous on Saturday.

2. The Rise of Neo-Banks

Traditional banks are seeing a mass exodus. Younger generations are flocking to Digital Banks (Chime, Monzo, SoFi) because they offer:

- Zero Fees: No monthly maintenance or overdraft fees.

- Early Payday: Getting your direct deposit two days early.

- Built-in Budgeting: AI that categorizes your spending automatically.

Common Financial Pitfalls to Avoid

Even with a budget, these “wealth-killers” can sneak up on you:

- Lifestyle Creep: As you earn more, you spend more. You get a $5,000 raise, and suddenly you “need” a more expensive car. Result? Your net worth stays at zero.

- The BNPL Loop: Buy Now, Pay Later services like Affirm or Klarna make it easy to buy $100 shoes for “$25 today.” But if you have five of these running at once, your paycheck is gone before it hits your account.

- Ignoring Inflation: Keeping $50,000 in a checking account earning 0.01% while inflation is 3.5% means you are literally losing money every year.

- The “Sunk Cost” Subscription: Paying for a gym you don’t go to because “I might go next week.” Cancel it. You can always sign up again.

Comparative Analysis: Traditional vs. Modern Strategies

| Concept | The “Old Way” (Pre-2020) | The “New Way” (2026) |

|---|---|---|

| Budgeting | Manual spreadsheets and receipts. | AI-driven apps with real-time tracking. |

| Emergency Fund | Kept in a big bank savings account (0.01%). | Kept in a High-Yield Savings Account (4.5%+). |

| Spending | Avoid all “frivolous” spending. | Mindful spending; prioritize joy, cut waste. |

| Credit Cards | Used for everything to get “points.” | Used strategically; high skepticism of high-interest debt. |

| Career | One job for 40 years. | Multiple income streams/Side hustles. |

Your 7-Step Action Plan for Financial Freedom

Ready to take control? Follow these steps in order:

- Calculate Your Net Worth: Total Assets (what you own) minus Total Liabilities (what you owe). This is your starting line.

- Track Every Penny for 30 Days: Use an app or a notebook. You cannot fix what you do not measure.

- Build a $1,000 “Starter” Emergency Fund: This stops you from using credit cards when the tire blows out.

- Attack High-Interest Debt: Anything over 7% interest (Credit cards, some personal loans) needs to go. Use the Avalanche method.

- Secure the Employer Match: If your job offers a 401(k) match, contribute enough to get the full amount. It’s a 100% return on your money—literally “free money.”

- Automate Your Savings: Set your bank to move 10% of your paycheck to savings the moment it arrives. If you don’t see it, you won’t miss it.

- Educate Continuously: Read one personal finance book a year. Stay curious about economic trends.

10 Frequently Asked Questions (FAQs)

1. How much should I save for an emergency fund?

Aim for 3 to 6 months of your must-have expenses (rent, food, basic utilities). If you are a freelancer, aim for 9 months.

2. Is all debt bad?

No. Debt with low interest that helps you build an asset (like a mortgage) can be “good debt.” High-interest debt (20%+) is almost always “bad debt.”

3. When should I start investing?

Today. The best time was 10 years ago; the second best time is now. Even $50 a month matters because of compound interest.

4. What is a “good” credit score?

Generally, anything above 700 is considered good. Above 800 is excellent and will get you the best interest rates.

5. Should I pay off debt or save first?

Build a small $1,000 emergency fund first. Then, pay off any debt with an interest rate higher than 7%. Once that’s gone, finish your full emergency fund.

6. What is the 50/30/20 rule?

It’s a budgeting framework: 50% for Needs, 30% for Wants, and 20% for Savings/Debt repayment.

7. Are digital banks safe?

Yes, as long as they are FDIC-insured (or the equivalent in your country). This protects your money up to $250,000 if the bank fails.

8. What is “Lifestyle Creep”?

It’s the tendency to increase your spending as your income increases, which prevents you from building actual wealth.

9. How do I improve my credit score fast?

Pay every bill on time and keep your credit card balances below 30% of your limit. Requesting a credit limit increase (without spending more) can also help.

10. Do I need a financial advisor?

If you have a complex estate or millions of dollars, yes. For most people starting out, following the basics of budgeting and low-cost index fund investing is enough.

Summary

Financial literacy isn’t about being a math genius. It’s about behavioral discipline. In 2026, the tools to manage your money are more powerful than ever, but the distractions (targeted ads, social media lifestyle pressure) are also stronger.

By mastering the five pillars—Budgeting, Saving, Debt Management, Credit, and Investing—you aren’t just managing numbers on a screen. You are buying back your time. You are ensuring that when “Future You” stands in front of that vending machine, you have exactly what it takes to press the button for Freedom.

Start now.