A Complete Guide to Protect Your Finances from Unexpected Expenses

Life is unpredictable. One day everything is going smoothly, and the next day an unexpected expense appears — medical bills, car repairs, job loss, or urgent family needs. When these situations happen without financial preparation, they can create serious stress and even debt.

This is where emergency fund planning becomes essential.

An emergency fund is a financial safety net designed to cover unexpected expenses without forcing you to borrow money or disrupt your financial goals. It gives you stability, peace of mind, and the ability to handle life’s surprises confidently.

Many people assume building an emergency fund requires a large income or complicated financial strategies. The truth is much simpler. With the right approach and consistent habits, anyone can build an effective emergency fund over time.

In this guide, you will learn:

- What an emergency fund is and why it matters

- How much emergency savings you really need

- Step-by-step emergency fund planning strategies

- Practical examples and charts

- Common mistakes to avoid

- Tips to build your fund faster

If you are still struggling with saving consistently, you should first read our guide on

Saving Money Faster.

By the end of this article, you will have a clear, practical plan to create and grow your emergency fund.

Table of Contents

- What Is an Emergency Fund

- Why Emergency Fund Planning Is Important

- Common Emergencies That Require Savings

- How Much Emergency Fund You Need

- Step-by-Step Emergency Fund Planning Guide

- Emergency Fund Savings Chart Example

- Real-Life Examples of Emergency Fund Success

- Where to Keep Your Emergency Fund

- Common Emergency Fund Mistakes

- Benefits and Effects of Having an Emergency Fund

- Tips to Build Your Emergency Fund Faster

- Frequently Asked Questions

What Is an Emergency Fund

An emergency fund is money set aside specifically for unexpected financial situations.

Unlike regular savings, this money is not used for shopping, vacations, or planned purchases. It is strictly reserved for real emergencies.

Examples include:

- Sudden medical expenses

- Car repairs

- Job loss

- Home maintenance

- Unexpected travel for family emergencies

Having an emergency fund means you can handle these situations without borrowing money or using credit cards.

Why Emergency Fund Planning Is Important

Emergency fund planning is one of the most important financial habits anyone can develop.

Without emergency savings, even a small financial problem can quickly become a major crisis.

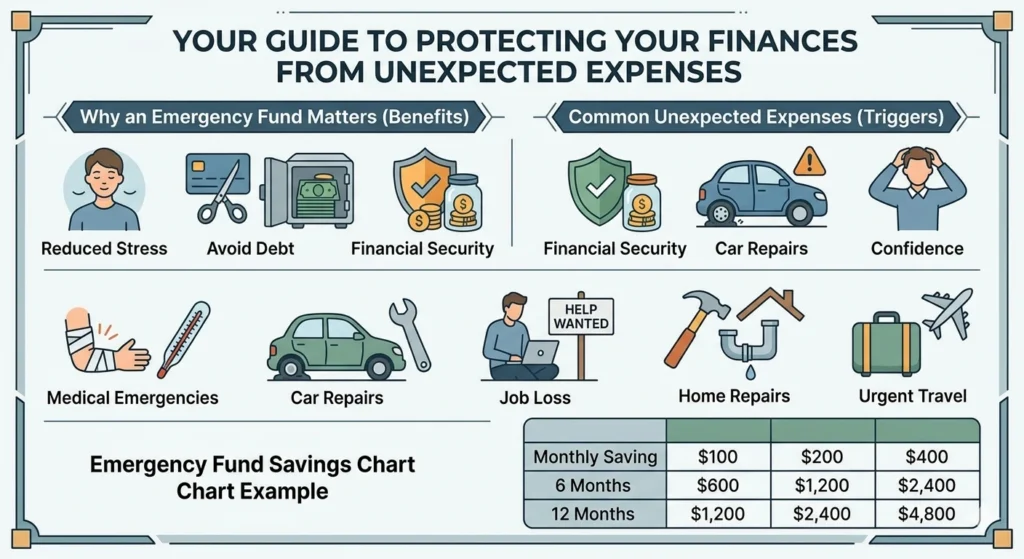

Key Benefits of Emergency Funds

Financial Security

An emergency fund protects your finances from unexpected disruptions.

Reduced Stress

Knowing you have money available for emergencies reduces anxiety and financial pressure.

Avoiding Debt

Instead of borrowing money during emergencies, you can rely on your savings.

Financial Independence

Emergency savings allow you to make better decisions without financial panic.

Common Emergencies That Require Savings

Many people underestimate how often emergencies occur. Some of the most common financial emergencies include:

- Medical emergencies

- Car breakdowns

- Unexpected home repairs

- Job loss or reduced income

- Family emergencies

- Urgent travel expenses

These situations can appear suddenly and require immediate financial resources.

How Much Emergency Fund You Need

Financial experts commonly recommend saving three to six months of living expenses.

However, the ideal amount depends on your financial situation.

Emergency Fund Levels

| Level | Savings Goal | Purpose |

|---|---|---|

| Beginner | $500 – $1,000 | Covers small emergencies |

| Intermediate | 3 months expenses | Basic financial protection |

| Advanced | 6 months expenses | Strong financial security |

Example:

If your monthly expenses are $1,500

| Months Covered | Savings Needed |

|---|---|

| 3 months | $4,500 |

| 6 months | $9,000 |

The key is starting small and building gradually.

Step-by-Step Emergency Fund Planning Guide

Building an emergency fund becomes much easier when you follow a structured approach.

Step 1: Calculate Your Monthly Expenses

First, determine your essential living costs.

Typical expenses include:

- Rent or mortgage

- Food

- Utilities

- Transportation

- Insurance

- Medical costs

Example:

| Expense | Monthly Cost |

|---|---|

| Rent | $700 |

| Food | $300 |

| Transport | $150 |

| Utilities | $120 |

| Insurance | $100 |

Total = $1,370

Step 2: Set a Realistic Savings Goal

Instead of saving the full amount immediately, create small milestones.

Example:

| Goal Stage | Target |

|---|---|

| First Goal | $500 |

| Second Goal | $1,000 |

| Third Goal | 3 months expenses |

Small milestones help maintain motivation.

Step 3: Create a Monthly Savings Plan

Determine how much you can save each month.

Example:

| Monthly Saving | Time to Reach $1,000 |

|---|---|

| $50 | 20 months |

| $100 | 10 months |

| $200 | 5 months |

Even small contributions make progress.

Step 4: Automate Your Savings

Automating transfers makes saving easier and consistent.

Example system:

Income → Automatic transfer → Emergency fund account

This prevents accidental spending.

Step 5: Protect the Emergency Fund

Your emergency fund should only be used for real emergencies.

Avoid using it for:

- Shopping

- Entertainment

- Vacations

Emergency Fund Savings Chart Example

Consistent saving can quickly build financial protection.

| Monthly Saving | 6 Months | 12 Months |

|---|---|---|

| $100 | $600 | $1,200 |

| $200 | $1,200 | $2,400 |

| $400 | $2,400 | $4,800 |

Over time, these savings grow into strong financial security.

Real-Life Example of Emergency Fund Success

Consider the story of Alex.

Alex earns $2,500 monthly and initially had no emergency savings.

After creating a plan:

| Strategy | Result |

|---|---|

| Reduced entertainment spending | Saved $120 |

| Cooked meals at home | Saved $150 |

| Side freelance work | Earned $200 |

Monthly emergency savings = $470

After one year, Alex saved:

$5,640

When a sudden car repair costing $900 occurred, Alex paid it without debt.

Where to Keep Your Emergency Fund

Your emergency savings should be safe and easily accessible.

Good options include:

High-Yield Savings Account

Offers interest while keeping funds accessible.

Separate Savings Account

Helps prevent accidental spending.

Money Market Account

Offers flexibility and modest interest.

Avoid placing emergency funds in risky investments such as stocks.

Common Emergency Fund Mistakes

Many people struggle to maintain emergency savings because of simple mistakes.

Using the Fund for Non-Emergencies

This weakens the purpose of the fund.

Saving Too Slowly Without a Plan

Random saving often leads to slow progress.

Keeping Funds in Cash at Home

Cash may be lost, stolen, or damaged.

Ignoring Small Contributions

Even small amounts add up over time.

Benefits and Effects of Having an Emergency Fund

An emergency fund creates powerful financial advantages.

Financial Effects

- Protection against unexpected expenses

- Reduced reliance on credit cards

- Increased financial stability

Emotional Effects

- Lower financial stress

- Greater confidence in handling challenges

- Improved financial discipline

Over time, emergency savings help create strong financial foundations.

Tips to Build Your Emergency Fund Faster

You can accelerate your savings with these strategies.

Reduce Unnecessary Spending

Cut expenses that do not add value.

Increase Income Sources

Consider side income such as:

- Freelancing

- Online services

- Small business activities

Save Windfalls

Use bonuses, gifts, or tax refunds to boost savings.

Track Progress Regularly

Monitoring progress keeps motivation strong.

Frequently Asked Questions

1. What is the purpose of an emergency fund?

An emergency fund helps cover unexpected expenses without borrowing money or disrupting financial stability.

2. How much should I save for emergencies?

Financial experts recommend saving three to six months of living expenses.

3. Can I start with a small emergency fund?

Yes. Even saving $500 or $1,000 provides protection against small emergencies.

4. Where should I keep my emergency savings?

A separate savings account or high-yield savings account is ideal.

5. Should I invest my emergency fund?

No. Emergency funds should remain safe and easily accessible.

6. How long does it take to build an emergency fund?

The time depends on your savings rate and financial situation.

7. What qualifies as an emergency?

Unexpected events such as medical bills, job loss, or urgent repairs.

8. Should I use my emergency fund to pay debt?

Only if the debt situation becomes a financial emergency.

9. What happens after reaching my emergency fund goal?

You can focus on investing or achieving other financial goals.

10. Can families also use emergency funds?

Yes. Emergency funds are even more important for families with dependents.

Final Thoughts

Emergency fund planning is one of the smartest financial decisions you can make. It protects your finances, reduces stress, and prepares you for life’s unexpected challenges.

Building an emergency fund does not happen overnight. However, with consistent saving habits and a clear plan, anyone can build strong financial protection over time.

Start small, remain disciplined, and gradually increase your savings. Over time, your emergency fund will provide the security and confidence needed to face financial uncertainties.

Once your emergency fund is ready, the next smart move is learning

Smart Debt Management.